This article is part of the series – Check your financial IQ. The aim of the series is to put together thoughts and practices that lead to better financial health. No matter how much money you earn, if you don’t have the financial IQ to handle the money, your wealth is not going to reach its full potential. Worse, your wealth could be actually diminishing every day if handled poorly. So education on personal finance is very important and if done right, it will lead to sustainable prosperity that many people crave.

Choosing between renting and buying

This scenario is when you are already living in a rented place (or plan to) and you are also open to considering buying the house too. Many people argue that if you can afford it, you should always buy a house instead of rent since the money paid to landlord is basically sunk cost. This argument is fundamentally flawed and incorrect. There can be many scenarios where renting a house is better than buying even from purely monetary perspective. First, let’s try to look at this problem analytically (we will discuss other factors later on). That is if you were to choose between these two options just on the basis of monetary benefit, then you need to consider the following:

- Mortgage: Unless you are buying the property outright, you need to consider the rate of interest the bank is going to charge you for the home loan. If your credit score is good, you can get a good bargain. On the contrary, having a poor credit score can lead to higher rates and even rejection. Even if you have the money to buy the house yourself, sometimes it is a good idea to get a loan from the bank because

- If the offered rate of interest is low, you can potentially do better by smart investing. For example, if the mortgage rate is 6%, and you are fairly confident of earning 10% in stocks, it is better to put your money there and get a loan for the house.

- Sometimes, you can get a tax rebate when you get a home loan. The rules vary across countries and also depends on individual’s current income situation. But you should calculate this benefit if available.

- Lastly, the banks usually do a legal check for the house to be mortgaged. This could be a good thing for you in case the construction is illegal. Please note that you should do a separate check on your own anyways by consulting a lawyer. If there is an issue with the house in future, bank would still recover money from you.

- Property price appreciation: You need to consider what is the expected increase/decrease in the price of the property over the years if you are going to buy a house instead of renting. While at first, it may seem that if you are buying a house to live yourself, this should not be a factor at all. However to compare it with the rent scenario we need to calculate the future value of the house as we will see later. It can understandably difficult to calculate the appreciation. After all, we are not wizards. But if you do your homework well, it can be reasonably estimated. This is where your judgement comes in. All I can say is that people are usually over optimisitc when it comes to expected returns from a house. I personally do some area wide research myself, look at historical trends, upcoming projects, ask friends, broker and then take an average of all the inputs. Finally, I reduce the % a bit to be on the safer side.

- Maintainence cost: Property needs regular maintainence, and maintainence costs money. This would include the cost of repairs, paint jobs etc. This would also include the maintainence charges levied by the society/developer if applicable. You can set it as a fixed % per year and subtract it from the property price appreciation for the purpose of calculation.

- Rent increment: If you go for renting instead of buying, you not only need to calculate the current rent amount, but also the yearly increase over a period of time. This should be relatively easier to do since rent increments are usually non-volatile and well known for a given area. Unless of course something unpredictable happens in which case the price of a bought house would also fluctatute accordingly so you can ignore that.

- Cost of money: For the comparison calculation, we need to know the cost of money. Or an expected return which you usually get from a safe investment like government bonds. You can also use inflation rate here. The point here is to get a rate which we can use to calculate the future value of your rent or EMI amount.

How to do the actual calculation for comparison

We have seen the parameters needed for doing an analytical comparison between rent and buy. Let’s get our hands dirty do some math now.

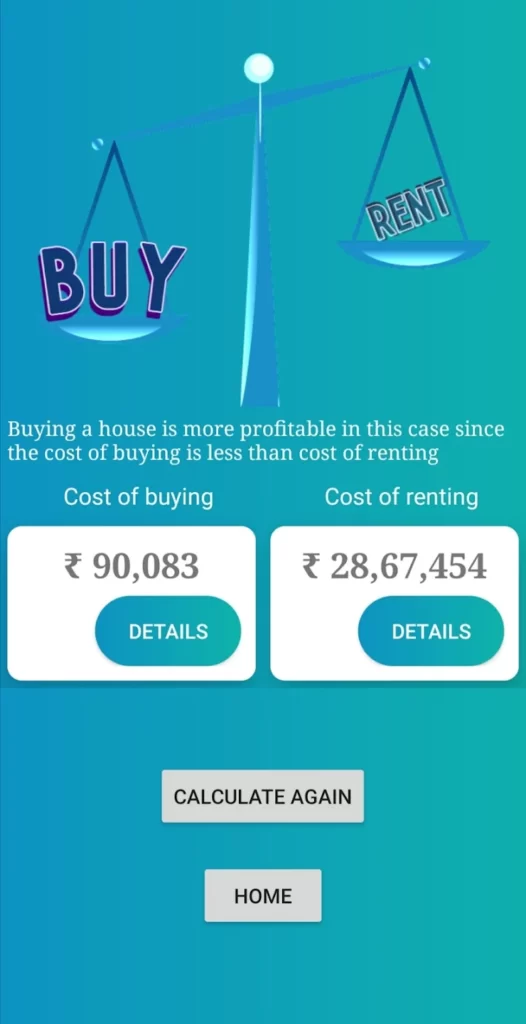

Note: This can be a bit boring and complicated if you are out of practise or simply don’t care. I have created an Android app specifically for the purpose of making this comparison easier. Check out Rent vs Buy section in House Genie app on the play store.

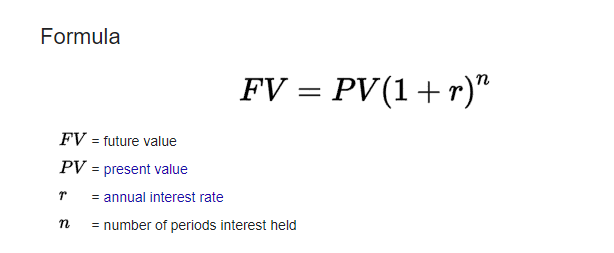

To do the comparison, you need to calculate cost of buying and cost of renting. Also the formula used for calculating the future value of any sum is:

Cost of buying a house

Consider a hypothetical scenario where you buy the house now and then sell your house after a set period of time, let’s say 20 years. The net cost of owning the house is total of future value of EMI and downpayment minus the future sale price of the house. The future sale price is calculate from the property appreciation rate. You also need to adjust the tax benefit you get from the EMI payment. For calculating the future value of any sum, we use the cost of money or inflation rate as a proxy. Note that time period for the future value calculation of the EMI would depend on the date of EMI and will be different on each payment, so this whole calculation is tedious to perform by hand.

a) Sale price of the house = Future value of current buy price using the rate of house appreciation

b) Cost of EMI = Sum of future values of all the EMIs paid at corresponding time period, adjusted for tax benefit

c) Cost of downpayment = Future value of initial downpayment using risk free rate

Cost of buying = (b) + (c) – (a)

Cost of renting a house

We use the same reference period as above for calculating this cost (20 years in this example). Cost of renting is the sum of the future values of rent payment using the risk free rate. Note that the time period will be different for each rent payment and the rent itself will change each year according the estimated rate of rent increment.

So there you are. You now know the estimated cost of buying vs estimated cost of renting. Whichever one is lower is a better choice from a purely monetary perspective. You can save yourself from all this pain and use the app which I have created. Some screenshots from the app

Other factors to consider before making the decision to rent or buy a house

So far we have only seen the comparison from a purely analytical/monetary perspective. But in real life there are a lot more factors to consider that are subjective and depends on the individual’s choice or preference.

Some points in favor of buying a house:

- Owning a house gives a sense of security that you have a roof over your head.

- No need to struggle moving from place to place when landlord asks you to vacate for whatever reasons.

- Can be a good investement asset if you are lucky and did the research well.

- Gives you a freedom that sometimes lacks in a rented place. Some landlords/neighbor treat the tenants as 2nd class citizens.

Some points in favor of renting a house:

- Sometimes due to nature of the job, you have to move around a lot and renting becomes indispensable.

- No need to worry about house maintainence and related expenses. Cost of rent is fixed which means a predictable cash outflow.

- No need to worry about making a bad decision or being unlucky to buy a house that you regret later on for whatever reasons.

- Move around and explore with no strings attached. For travel lovers, you get to enjoy large number of places if the job permits of course.

I hope this article was helpful. Would love to see your comments on the points I may have missed.

Important Disclaimer: I am not a financial advisor and the information and resources on this website should not be construed as financial advice. While I have tried my best to provide meaningful information as accurately as possible, use your own judgment or take the help of a professional who can advise based on your particular needs and situation.